How do payment processors make money

In today's fast-paced digital economy, payment processors play a critical role in facilitating the seamless transfer of funds between consumers and businesses. Whether it's an online purchase, a swipe at a retail store, or a recurring subscription, payment processors ensure that transactions happen swiftly and securely. Without them, businesses would struggle to accept a wide range of payment methods, hindering their growth and customer reach.

But have you ever wondered, how do payment processors make money?

While the technology behind payment processing may seem straightforward, these companies generate revenue through a variety of channels. From transaction fees charged on every sale to additional fees for services like fraud prevention, payment processors have created a complex system of charges that fuel their profitability. This blog will explore the key revenue streams — including transaction fees, monthly fees, and value-added services — that enable payment processors to thrive in the ever-evolving landscape of electronic payments.

Primary Revenue Source – Transaction Fees

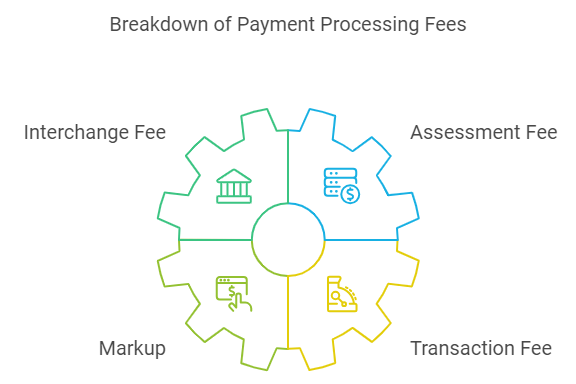

1.1 Breakdown of Transaction Fees

The primary way payment processors generate income is through transaction fees. Every time a consumer makes a payment using a credit or debit card, the merchant incurs a cost for processing that transaction. These fees are typically a combination of several components:

- Interchange Fee: This fee is charged by the acquiring bank (the merchant’s bank) and is often the largest component of the transaction cost. The interchange fee is a percentage of the total transaction and varies based on factors such as the type of card used (credit, debit, or premium), the transaction amount, and the industry in which the merchant operates. For example, a luxury retailer may have a higher interchange fee compared to a grocery store because of the transaction value and perceived risk.

- Assessment Fee: This is a smaller percentage fee charged by the card networks like Visa, Mastercard, or American Express. It covers the costs associated with maintaining the card network’s infrastructure and security. The assessment fee is typically consistent across all merchants but varies slightly between different card networks.

- Markup: The payment processor adds a markup to the transaction, which is its primary source of profit. This markup can vary depending on the size of the merchant’s business, the volume of transactions processed, and the risk profile of the merchant’s industry. Smaller businesses tend to pay higher markups because they have less negotiating power compared to large enterprises with higher transaction volumes.

- Transaction Fee: In addition to the percentage-based charges, payment processors also impose a fixed fee per transaction. This is usually a small, set amount (e.g., $0.15 or $0.30 per transaction), regardless of the size of the transaction. It compensates the processor for the technical costs of processing the payment.

1.2 Example of Transaction Fee Calculation

Let’s consider a hypothetical transaction to see how these fees work in practice. Suppose a customer makes a $100 purchase at an online store, and the store's payment processor charges a transaction fee of **3.5% + $0.15** per transaction. Here’s how the fees break down:

- Interchange Fee: 2.0% of the transaction amount, which equals $2.00.

- Assessment Fee: 0.15% of the transaction, which equals $0.15.

- Markup: 1.0%, which adds up to $1.00.

- Transaction Fee: A fixed fee of $0.15.

In total, the merchant would pay $3.30 in fees for the $100 transaction. This amount includes the interchange fee, assessment fee, markup, and the fixed transaction fee. As a result, the payment processor earns part of that fee through the markup and the fixed transaction fee, while the interchange and assessment fees are passed on to the banks and card networks.

While 3.5% may seem small, these fees add up quickly, especially for businesses that process thousands of transactions daily. For the payment processor, every fraction of a percentage translates into significant revenue over time.

Other Fees That Contribute to Revenue

Beyond transaction fees, payment processors also earn revenue from various other fees that merchants incur for using their services. These fees are often recurring or related to specific services that merchants rely on for the smooth operation of their payment processing systems. Let’s break down some of these additional charges.

Monthly Fees

Payment processors typically charge merchants a monthly fee for maintaining their merchant accounts. This fee covers the basic infrastructure and support provided by the processor, such as account management, customer service, and general maintenance. These fees can vary depending on the size of the merchant and the services included in their plan. For smaller businesses, this may be a flat fee, whereas larger businesses may negotiate different terms based on their transaction volume.

By charging monthly fees, payment processors secure a steady and predictable revenue stream, even if a merchant's transaction volume fluctuates throughout the year.

Early Termination Fees

Merchant agreements with payment processors often come with contractual obligations that last for a set period, such as one or two years. If a merchant decides to terminate their contract early, they are usually subject to early termination fees (ETFs). These penalties are designed to compensate the processor for the lost business and the cost of setting up the account.

For the payment processor, early termination fees provide an additional safeguard against potential revenue loss. While most merchants don’t expect to pay these fees, ETFs can become a significant source of income, especially when merchants switch processors before their contracts expire.

PCI Compliance Fees

Payment processors are responsible for ensuring that their merchants comply with the Payment Card Industry Data Security Standard (PCI DSS), which is a set of security standards designed to protect sensitive cardholder information. To ensure compliance, processors charge merchants PCI compliance fees, which can be either monthly or annual.

These fees help cover the cost of security assessments, system updates, and other measures necessary to maintain PCI compliance. Non-compliance could result in costly fines or data breaches, so many merchants are willing to pay these fees for peace of mind. For payment processors, these fees represent an additional revenue stream tied to the ever-growing importance of data security in online and in-person transactions.

Statement Fees

Each month, merchants receive a detailed statement from their payment processor, summarizing their transaction activity and the fees they’ve incurred. Some payment processors charge a statement fee for generating and delivering this billing information. This fee is typically modest but adds up over time, especially for processors with a large merchant base.

By charging statement fees, payment processors generate additional income from what is essentially a necessary service for merchants to keep track of their expenses. Although many merchants have shifted to digital statements, these fees persist, adding another layer of revenue to the processor's business model.

These additional fees, while often smaller than transaction fees, are a critical part of a payment processor’s revenue model. They provide steady income and ensure that processors can cover operational costs while maintaining profit margins, even beyond transaction-related earnings.

Value-Added Services

In addition to transaction and account maintenance fees, payment processors offer a range of **value-added services** that provide merchants with additional tools and features to improve their business operations. These services not only help merchants streamline their processes but also generate extra revenue for the payment processors.

Fraud Detection and Prevention Tools

With the rise of digital payments, security has become a top priority for businesses. Payment processors offer **fraud detection and prevention tools** that help merchants safeguard against fraudulent transactions, chargebacks, and potential breaches. These tools often include real-time monitoring, advanced analytics, and machine learning algorithms that flag suspicious activity.

By offering these security solutions, processors can charge merchants additional fees, either as a monthly subscription or on a per-transaction basis. Merchants are often willing to pay for these tools because the cost of fraud, both financially and reputationally, can be far higher than the fee for preventive services.

Chargeback Management

Chargebacks occur when a customer disputes a charge and requests a refund through their bank. Handling chargeback disputes can be time-consuming and costly for merchants, and many payment processors offer chargeback management as a service. This service includes helping merchants navigate the complex chargeback process, gather necessary documentation, and dispute claims.

By offering this assistance, payment processors can charge merchants for each case they help resolve or offer it as part of a premium package. Chargeback management services not only ease the burden on merchants but also generate significant revenue for processors as disputes and fraud continue to rise in the digital payments space.

Loyalty and Rewards Programs

To help merchants increase customer engagement and repeat business, some payment processors provide **loyalty and rewards programs**. These programs allow merchants to offer customers incentives such as points, discounts, or cash-back rewards for repeat purchases.

For payment processors, offering these services represents an opportunity to earn additional revenue, either through monthly service fees or by taking a percentage of the increased transaction volume these programs generate. Loyalty programs are a win-win, as they help merchants attract and retain customers while allowing processors to profit from the extra activity.

Data Analytics and Reporting

Payment processors also offer data analytics and reporting services that provide merchants with insights into their transaction data, customer behavior, and sales trends. These advanced analytics tools can help businesses make informed decisions about inventory management, marketing strategies, and overall business performance.

By providing merchants with detailed reporting and data-driven insights, payment processors can charge for these premium services. Merchants, in turn, are willing to pay for actionable data that can help them optimize operations, boost sales, and reduce costs, creating a significant source of additional revenue for processors.

Emerging Trends in the Payment Processing Industry

As technology and consumer behavior continue to evolve, so do the business models of payment processors. New trends are reshaping the way payment processors generate revenue, pushing them to adapt and innovate.

Cash Discount or Zero-Fee Processing Models

In response to rising transaction fees, some merchants have adopted cash discount or zero-fee processing models, where they pass the processing fees on to customers as a surcharge. In this model, the merchant advertises a lower price for cash payments, while card payments incur a small surcharge to cover processing costs.

Payment processors benefit from this model because it allows them to maintain their revenue streams while keeping merchants satisfied by reducing their out-of-pocket processing costs. Although the customer pays the surcharge, the processor still profits from transaction fees, creating a more merchant-friendly arrangement.

Adapting to New Technologies

As new technologies emerge, payment processors must continuously evolve to stay competitive. Innovations like blockchain, mobile payments, and fintech advancements are reshaping the payment processing landscape.

- Blockchain has the potential to streamline transactions by eliminating intermediaries, reducing costs, and improving security. Payment processors may develop blockchain-based solutions to capitalize on this technology.

- Mobile payments are becoming increasingly popular with the rise of platforms like Apple Pay, Google Wallet, and peer-to-peer payment apps. Payment processors are tapping into this trend by integrating mobile-friendly solutions that appeal to merchants and consumers.

- Fintech advancements such as open banking, AI-powered payment systems, and decentralized finance (DeFi) could revolutionize how payment processors operate, prompting them to offer new services that meet changing consumer demands.

By staying at the forefront of these technological advancements, payment processors can unlock new revenue streams and future-proof their business models in an increasingly digital economy.

Conclusion

Payment processors generate income through a diverse range of revenue streams. While transaction fees—consisting of interchange fees, assessment fees, markups, and fixed transaction charges—remain their primary source of income, it’s clear that these companies have developed multiple ways to boost their profitability. From monthly account maintenance fees to specialized charges like PCI compliance and early termination fees, processors ensure steady income beyond each transaction.

In addition to these traditional revenue sources, value-added services such as fraud detection, chargeback management, loyalty programs, and data analytics have become increasingly important. These services not only enhance the offerings for merchants but also serve as significant profit generators for payment processors, as businesses are willing to pay for the additional security, insights, and customer engagement tools they provide.

Looking ahead, the payment processing industry is poised for further growth and transformation, driven by emerging trends such as zero-fee processing models and technological advancements like blockchain and mobile payments. As these trends continue to evolve, payment processors will need to adapt their business models to maintain a competitive edge, ensuring that they remain essential players in the digital economy. By embracing innovation and continuing to expand their fee-based and service-driven revenue streams, payment processors are well-positioned to thrive in the future of global commerce.